Chapter 18Limiting Loan Loss Probability Distribution

Written in 1989; printed in Derivatives Pricing: The Classic Collection, P. Carr (ed.). London: Risk Books, 2004.

The cumulative probability that the percentage loss on a portfolio of n loans does not exceed ![]() is

is

where ![]() are given by an integral expression in Oldrich Vasicek's memo, “Probability of Loss on Loan Portfolio,” February 1987 (Chapter 17 of this volume). The substitution

are given by an integral expression in Oldrich Vasicek's memo, “Probability of Loss on Loan Portfolio,” February 1987 (Chapter 17 of this volume). The substitution

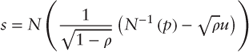

in the integral gives ![]() as

as

where

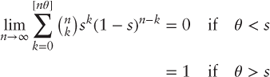

By the law of large numbers,

and therefore the cumulative distribution function of loan losses on a very large portfolio is

This is a highly skewed distribution. Its density is

Its mean, median, and mode are given by

The α-quantile, ...

Get Finance, Economics, and Mathematics now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.