AUTHORITATIVE LITERATURE USED IN AUDITING (STUDY OBJECTIVE 4)

The work of an auditor must be conducted in accordance with several sources of authoritative literature, as described next.

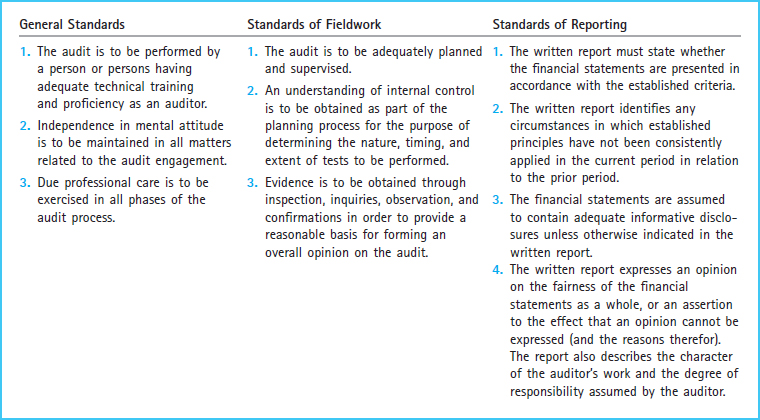

Generally accepted auditing standards (GAAS) are broad guidelines for an auditor's professional responsibilities. These ten standards are divided into three categories that include general qualifications and conduct of an auditor (general standards), guidelines for performing the audit (standards of fieldwork), and requirements for the written report communicating the results of the audit (standards of reporting). Exhibit 7-1 summarizes these standards by category.

Exhibit 7-1 Generally Accepted Auditing Standards

GAAS provides a general framework for conducting quality audits, but this framework is not specific enough to provide useful guidance in the actual performance of an audit engagement. For such detailed guidance, auditors rely upon standards issued by the Public Company Accounting Oversight Board, the Auditing Standards Board, the International Auditing and Assurance Standards Board, the Internal Auditing Standards Board, and the Information Systems Audit and Control Association.

The Public Company Accounting Oversight Board (PCAOB) was organized in 2003 for the purpose of establishing auditing standards for public companies in the United States. These standards are to serve as interpretations ...

Get Accounting Information Systems: The Processes and Controls, 2nd Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.