Module 17

Statement of Cash Flows

Statement of Cash Flows

Purpose of Statement

Summarizes sources and uses of cash and cash equivalents

Classifies cash flows into operating, investing, and financing activities

Cash Equivalents

Easily converted into cash (liquid)

Original maturity ≤ three months

Format of Statement

| Cash provided or (used) by operating activities | |

| ± | Cash provided or (used) by investing activities |

| ± | Cash provided or (used) by financing activities |

| = | Net increase or (decrease) in cash and cash equivalents |

| + | Beginning balance |

| = | Ending balance |

Inputs to the Cash Flow Statement

Each item on the balance sheet (change from prior year) and income statement must be accounted for. In general:

Operating activities:

- Income statement items/adjustments (e.g., sales)

- Current assets and current liabilities (e.g., accounts receivable)

Investing activities:

- Noncurrent assets (e.g., building)

Financial activities:

- Noncurrent liabilities and equity (e.g., bank loan, stock)

Some changes do not involve cash (equipment purchased with stock), and some do not follow the general rule (e.g., dividends payable is a current liability, but since it is the result of stock ownership, its adjustment will appear in financing activities instead of operating activities).

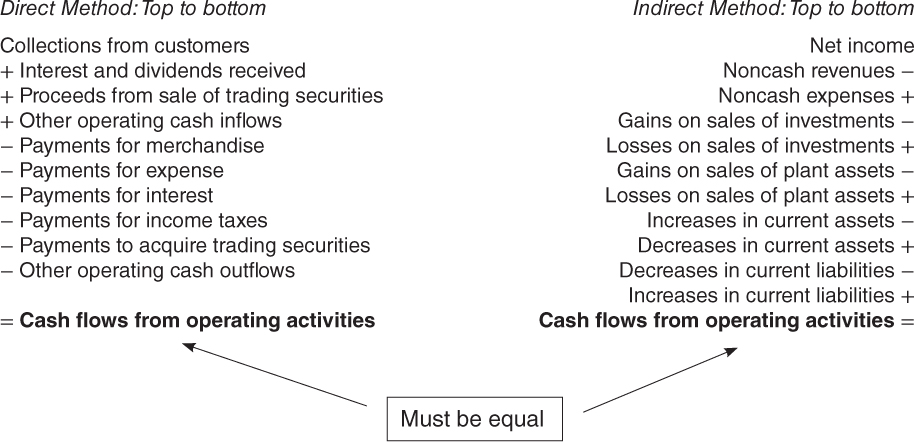

Operating Activities

Components of Direct Method

| Collections from customers (plug) | xxx ... |

Get Wiley CPAexcel Exam Review 2015 Focus Notes: Financial Accounting and Reporting now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.