Module 7: Audit Sampling

Overview

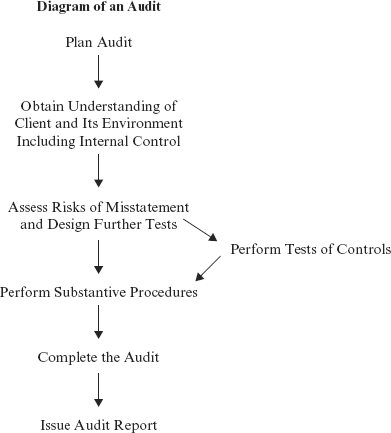

Sampling is essential throughout audits as auditors attempt to gather sufficient appropriate audit evidence in a cost efficient manner. The following “Diagram of an Audit” was originally presented in the auditing overview section.

A. Basic Audit Sampling Concepts

B. Sampling in Tests of Controls

C. Sampling in Substantive Tests of Details

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

Audit sampling is used for both tests of controls (attributes sampling) and for tests of details of transactions and balances (usually, variables sampling). In both attributes sampling and variables sampling, the plans may be either nonstatistical or statistical. The chart at the bottom of this page summarizes methods of audit sampling.

Audit sampling has been tested on most recent auditing examinations, usually in the form of multiple-choice questions. One might anticipate additional questions dealing with concepts such as sampling risk, nonsampling risk, tolerable misstatement1, and the projection of sample results to an overall population. Also, as in the past, one might expect exam questions dealing with the relationships between statistical concepts and basic audit concepts such as assessing control risk, materiality, and audit decision making. One might expect a portion of a simulation to require ...

Get Wiley CPAexcel Exam Review 2014 Study Guide, Auditing and Attestation now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.