APPENDIX A

Central Limit Theorem-Plausibility Argument

If a path begins at a point x0 then the initial distribution over x is the Dirac delta distribution, which means merely that the path has probability 1 of being located exactly at the starting point, expressed as

p(x; t = 0) = δ(x − x0).

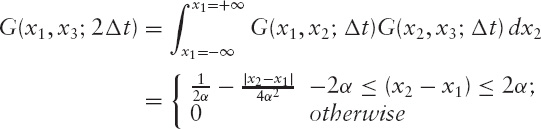

Then use a square shock, meaning that the distribution is convoluted with a square of width 2α and height 1/(2α),

and the new distribution is then a square. Then convolute again and the new distribution is a triangle,

and so on. Now, in more general terms, let the shock be some function f(x), not necessarily a square. Fourier transform the function to get f(p), and expand it as follows:

f(p) = a0 exp(−a2(p − p0)2 + a3(p − p0)3 + · · ·)

about its maximum, at p0. This expansion is meaningful as long as the derivative of f(p) is zero and continuous at p0 and the second derivative of f(p) is continuous and negative (i.e., a2 > 0). Then take the N-th power of this, to get the Fourier transform of the operator that gives us the N-step distribution:

Now the argument is that because the first term looks like the Fourier transform of a Gaussian of standard deviation

and for a particular standard deviation, ...

Get The Mathematics of Derivatives: Tools for Designing Numerical Algorithms now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.