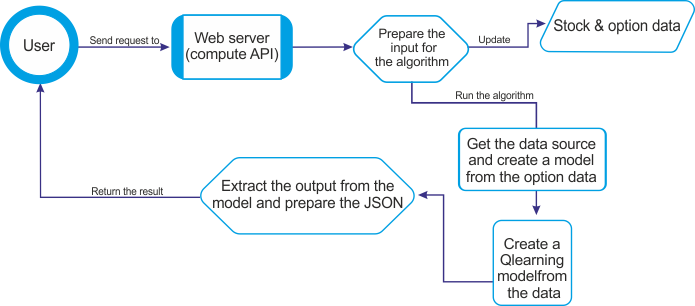

The goal of this project is to create an options trading web application that creates a QLearning model from the IBM stock data. Then the app will extract the output from the model as a JSON object and show the result to the user. Figure 10, shows the overall workflow:

Figure 10: Workflow of the options trading Scala web

The compute API prepares the input for the Q-learning algorithm, and the algorithm starts by extracting the data from the files to build the option model. Then it performs operations on the data such as normalization and discretization. It passes all of this to the Q-learning ...