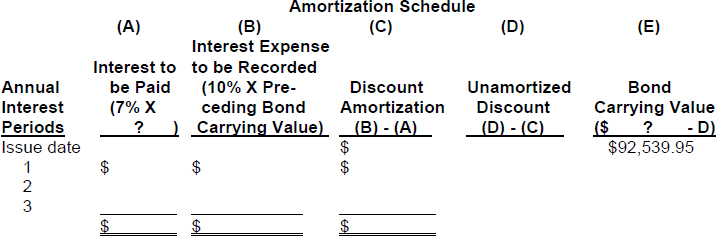

*EXERCISE 10-12

Purpose: (L.O. 10) This exercise will illustrate the computations and journal entries for a bond when the effective-interest method of amortization is used.

The Jan Larsen Corporation issued bonds with the following details:

| Face value | $100,000.00 |

| Contractual interest rate | 7% |

| Market interest rate | 10% |

| Maturity date | January 1, 2017 |

| Date of issuance | January 1, 2014 |

| Issuance price | $92,539.95 |

| Interest payments due | Annually on January 1 |

| Method of amortization | Effective-interest |

| End of annual reporting period | December 31 |

Instructions

- (a) Complete the amortization schedule for these bonds which appears below.

- (b) Prepare the journal entries to record:

- (1) The issuance of the bonds on January 1, 2014.

- (2) The adjusting entry(s) at December 31, 2014.

- (3) The payment entry on January 1, 2015. (Assume reversing entries are not used.)

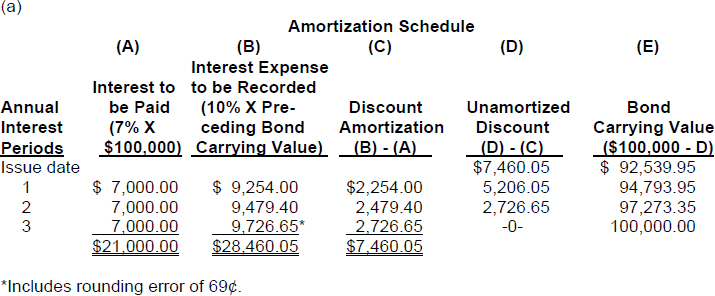

SOLUTION TO EXERCISE 10-12

Explanation: Interest to be paid (stated interest) is determined by multiplying the face value ($100,000) by the contractual interest rate (7%). Interest expense is computed by multiplying the carrying value at the beginning of the interest period by the effective-interest rate (10%). The amount of discount amortization for the period is the excess of the interest expense over the stated interest ...

Get Problem Solving Survival Guide to accompany Financial Accounting, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.