5.1 General Tax Rules for Property Sales

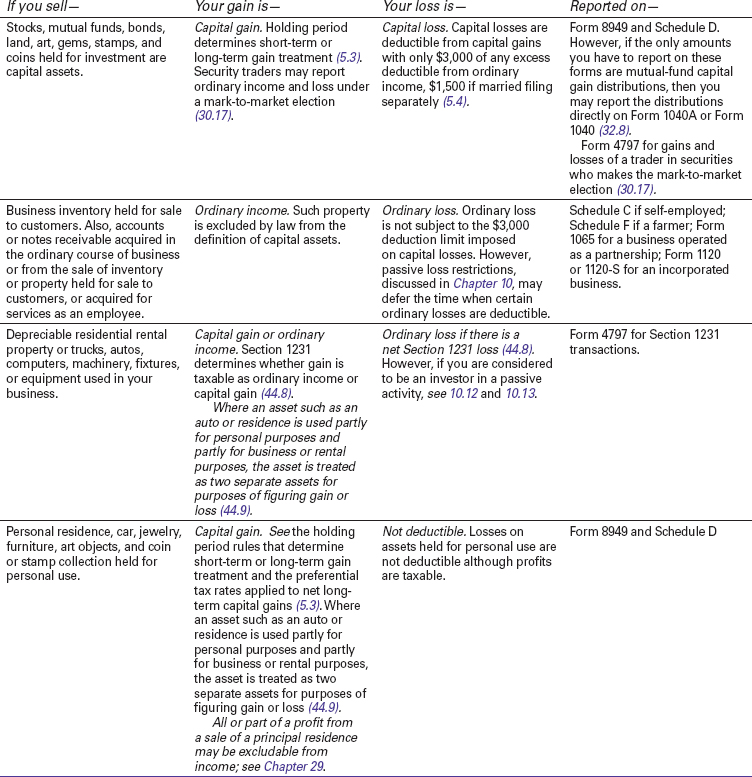

1. Property is classified according to its nature and your purpose for holding it; see 5.2, Table 5-1, and holding period rules at 5.3 and 5.9–5.12.

Table 5-1 Capital or Ordinary Gains and Losses From Sales and Exchanges of Property

2. Sales of capital assets must generally be reported on Form 8949, with Part I used for short-term gains and losses and Part II for long-term gains and losses (5.3). You must indicate on Form 8949 if you received a Form 1099-B from a broker showing your basis in securities sold. You may need to file multiple Forms 8949 depending on how basis was reported on Form 1099-B. Total amounts for sales price and basis are transferred from Form 8949 to Schedule D of Form 1040. On Schedule D you net short-term and long-term transactions to figure your net gain or loss for the year and, if you have net long-term gain, you are directed to the appropriate IRS worksheet for computing your tax liability taking into account the favorable capital gain rates, as discussed in the next paragraph. Filing Form 8949 or Schedule D may not be necessary if your only capital gains are from a mutual fund or REIT (32.8).

3. If you sell property at a gain, the applicable tax rate depends on the classification of the property (see Table 5-1) and, in the case of capital assets, the period you held the property before sale. A capital gain ...

Get J.K. Lasser's Your Income Tax 2013: For Preparing Your 2012 Tax Return now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.