6.2. TESTING TECHNIQUES

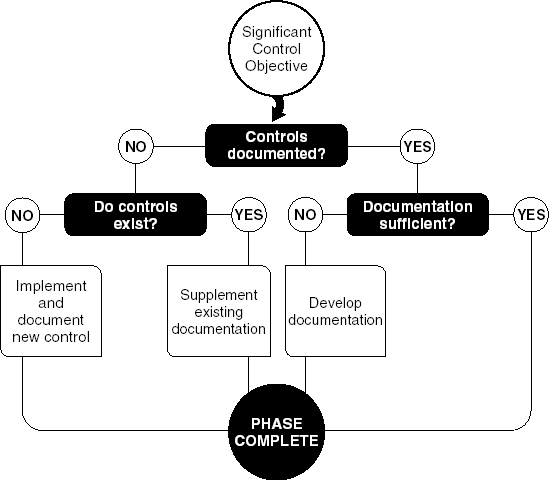

This chapter provides a comprehensive, integrated approach to testing and evaluating entity-level controls. Exhibit 6.1 summarizes the various testing techniques suggested and how these are used to gather evidence to support an assertion for each significant entity-level control objective.

Figure 6.1. ENTITY-LEVEL CONTROLS TESTING TECHNIQUES

6.2.1. Nature of Available Evidence

The effect that entity-wide controls have on the financial statements is indirect. It is nonlinear, subjective, and not easily quantified. Supporting an assertion on the effectiveness of entity-wide controls is challenging because the assertion cannot be verified by confirmation, inspection, and observation—that is, by the types of tests that auditors normally consider to be the most reliable. Entity-wide controls are not transaction oriented, so you will not be able to test their effectiveness by performing transactions-based tests. The techniques described here are the most effective way to gather evidence to support an assertion about entity-wide controls.

6.2.2. Survey and Inquiries of Employees

Surveys are an effective way of collecting information that should come directly from people, not documents. In particular, surveys are essential to evaluate whether an entity's culture and personnel policies create an environment that enables the effective functioning of activity-level ...

Get How to Comply With Sarbanes-Oxley Section 404: Assessing the Effectiveness of Internal Control now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.