23.2 Market Basics and Size

23.2.1 FX Outright Forwards and Futures

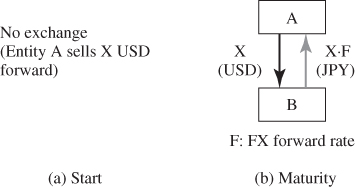

An outright FX forward contract is a contract where two parties agree to deliver, at a fixed future date, a specified amount of one currency in exchange for another. The only difference from an FX spot contract is that an FX forward is settled on any preagreed date, which is 3 or more business days after the deal, while the FX spot is settled or delivered on a date no later than 2 business days after the deal.

Suppose a US company purchases a product from a Japanese company with payment of 1 million yen due in 90 days. This importer owes yen for future delivery. The current price of the yen is assumed to be 100 yen per dollar. Over the next 90 days, however, the yen might rise against the US dollar, raising the US dollar cost of the product. This importer can avoid this FX risk by entering into a 90-day forward contract with a bank at the price of, say, 98 yen per dollar, which corresponds to the FX forward rate (see Fig. 23.1 for illustration of outright forward contract). In addition to the hedging purpose as shown in this example, FX forward contracts can also be used for speculative trades that take on FX risk by betting on a rise or fall of future FX rates.

Figure 23.1 Outright FX forward.

FX forward contracts are traded over the counter (OTC), that is, a network of banks and brokers, which allows customers ...

Get Handbook of Exchange Rates now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.