APPENDIX A

Crystal Ball’s Probability Distributions

This appendix lists a short description of each distribution in the Crystal Ball gallery along with its probability distribution function or probability density function (PDF), cumulative distribution function (CDF) where available, mean, standard deviation, and typical uses. For more information about these distributions, see Evans, Hastings, and Peacock (1993), Johnson, Kemp, and Kotz (2005), Johnson, Kotz, and Balakrishnan (1994), Law and Kelton (2000), or Pitman (1993).

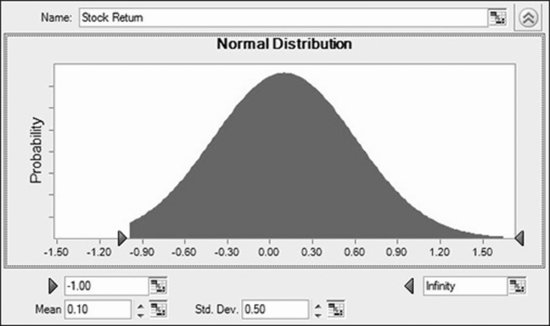

All of Crystal Ball’s distributions can be truncated on either or both ends to adapt to the circumstances of your model. Truncation is accomplished by entering the desired values in the truncation fields. For example, in Figure A.1, the normally distributed total return on a stock with nominal mean return 10 percent and nominal standard deviation 50 percent is truncated at −100 percent to reflect the limited liability of stock ownership.

FIGURE A.1 Normal distribution of a stock return truncated at −100 percent to reflect the limited liability of stock ownership.

When Crystal Ball truncates a distribution, the probability distribution is rescaled so that the total probability is 100 percent that a value will be generated within the range defined by the truncation points. For example, a random variable generated from the distribution shown in Figure A.1 has ...

Get Financial Modeling with Crystal Ball and Excel, + Website, 2nd Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.