15.4. EVIDENCE ON SYNERGY—VALUE CREATED AND ADDED

In the preceding section, we showed that synergy can have considerable value in many acquisitions, either by increasing expected cash flows or by lowering discount rates. In this section, we consider a question that is just as critical from the acquirer's standpoint, which is the price that should be paid for synergy. We begin by looking at the evidence on the existence of synergy both at the time of the merger announcement and in the aftermath. We follow up by laying out a framework for assessing how best to fairly share the benefits of synergy and where the odds are greatest for succeeding with a synergy-based acquisition strategy.

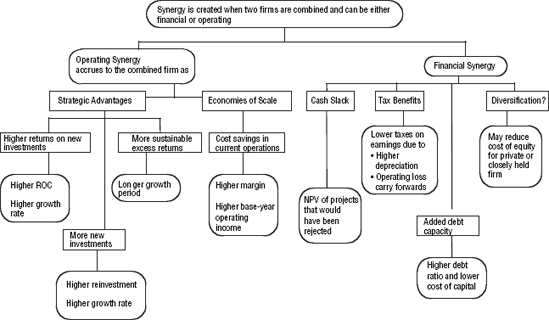

Figure 15.2. Synergy and Value

15.4.1. Evidence on Synergy

There are two ways we can evaluate the existence of the synergy. The first is on a forward-looking basis, by looking at market reactions to acquisition announcements and gauging what the expected synergy value is and who gets the gains. The second is to track mergers after they occur and evaluate the success of firms in delivering synergy gains.

15.4.1.1. Market Assessments at Time of Merger

Synergy is a stated motive in many mergers and acquisitions. Bhide (1993) examined the motives behind 77 acquisitions in 1985 and 1986 and reported that operating synergy was the primary motive in one-third of these takeovers.[] Do markets believe these ...

Get Damodaran on Valuation now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.