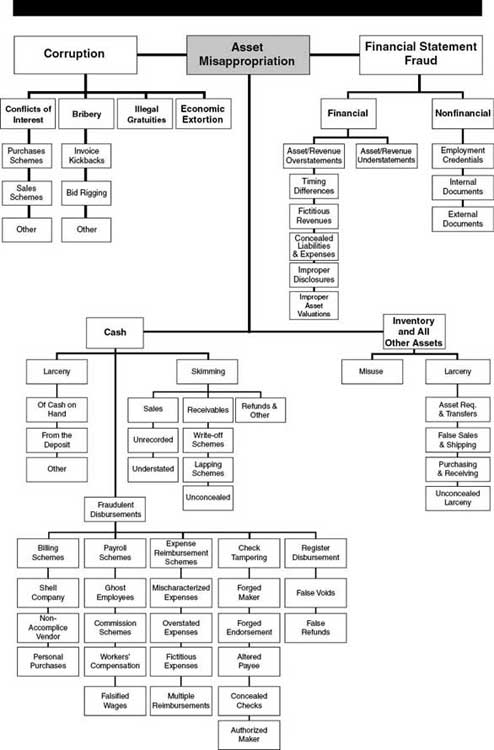

CHAPTER 2

Introduction to Asset Misappropriations

OVERVIEW

The purpose of this chapter is to provide an overview of the favorite target of occupational fraud offenders: the organization’s assets. Before defining assets, let us first learn what constitutes misappropriation. According to Black’s Law Dictionary,

misappropriation [is] the act of misappropriating or turning to a wrong purpose; wrong appropriation, a term that does not necessarily mean peculation, although it may mean that. The term may also embrace the taking and using of another’s property for sole purpose of capitalizing unfairly on good will and reputation of property owner.1

The definition in Webster’s is a little more pointed: “to appropriate wrongly (as by theft or embezzlement).”2 For our purposes, misappropriation includes more than theft or embezzlement. It involves the misuse of any company asset for personal gain. Therefore, employees using a company computer after hours for their own side business have not stolen an asset, but they have misappropriated it for their own benefit.

DEFINITION OF “ASSETS”

In commerce, the purpose of assets is to produce income. If a business produces oil, the rigs, trucks, and even the land are all assets. Should the business sell clothing, its merchandise and display cases are assets. Assets can be defined as “probable future economic benefits obtained or controlled by a particular ...

Get Corporate Fraud Handbook: Prevention and Detection, 4th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.