97

3

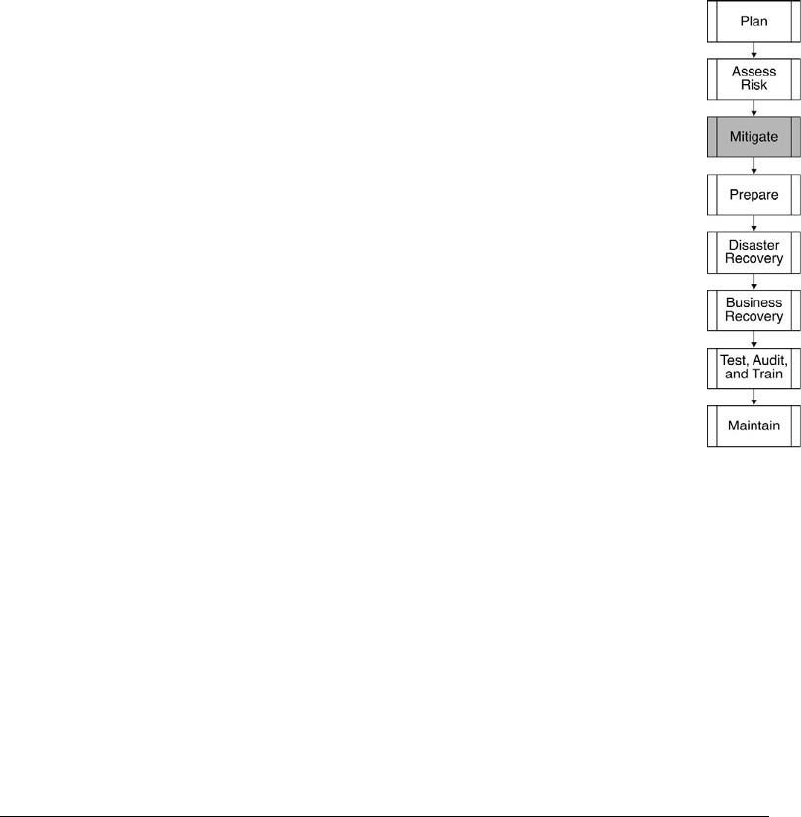

Mitigation Strategies

Migration Strategies

All organizations should prepare for emergency situations.

Part of this preparation process is a review of what is already

in place, what needs to be put in place, who needs to be

contacted when something happens, what they should do

when contacted, and so on. Many organizations have a

wide range of existing procedures for dealing with various

types of unusual situations. These procedures may have

been developed in response to a legal or regulatory require-

ment. This section will review what are considered the most

pertinent procedures for mitigating a disaster situation. It is

by no means an exhaustive list. The BCP should contain a

brief summary of each of these procedures, including the

issues that are relevant in the event of handling an emer-

gency disaster situation. Risk mitigation is a systematic

methodology used by senior management to reduce mission

risk and can be achieved through any of the following risk

mitigation options:

Risk Assumption. This is accepting the potential risk and either con-

tinuing to operating the IT system or implementing controls to lower

the risk to an acceptable level. Even if your procedures are aligned to

your risk assumptions, if your plans are based on the previously avail-

able amount of required resources, it is more than likely that these

requirements have increased. For example, renewal may not be an

option for contracts at alternative sites that are effective for only a

two-month period. After September 11, 2001, many businesses that

recovered operations at commercial “hot sites” found their subscribed

resources were insufficient for their actual needs.

98 Migration Strategies

Risk Avoidance. This is the making an informed decision to not

become involved in or otherwise avoid a risk situation by eliminating

the risk cause and/or consequence. For example, you could forgo cer-

tain functions of the system, or shut down the system when risks are

suspected or known.

Risk Limitation. This is the selective application of appropriate tech-

niques and management principles to reduce the likelihood of an

occurrence, its consequences, or both, limiting the risk by imple-

menting controls that minimize the adverse impact of a threat’s exer-

cising a vulnerability. For example, use supporting, preventive,

detective controls as part of a business continuity plan or emergency

response plans.

Risk Planning. This is the management of risk through the develop-

ment of a risk mitigation plan that prioritizes, implements, and

maintains controls. Uncertainty in life is a certainty. Our lives are in a

constant state of flux, family relations change, government constantly

enacts new and often conflicting laws, and our financial situation is

in a constant state of change. Notwithstanding the constant state of

change we live in, we all plan for the future. In planning for the unex-

pected, five criteria are generally considered:

1. Determine what unexpected events might occur. Many events are

reasonably foreseeable, such as the death of a loved one, divorce,

changes in the economy, financial reversal, and so forth.

2. Determine what “unexpected” events are likely to occur. For

example, if you are a stockbroker, syndicator, real estate devel-

oper, investment banker, physician, accountant, or attorney, there

is a substantial likelihood that you will be named in a lawsuit.

More than half of all marriages end in divorce (the other half end

in death of one of the parties).

3. Analyze the impact that unexpected events could have on your

tentative plans. For example, a savings and loan, into which you

put all of you money, may go broke; you can determine the effect

on your plans and make contingencies (e.g., don’t put more

money in one financial institution than can be federally insured).

4. In advance, plan alternatives in case an unexpected event occurs.

This is also referred to as “don’t put all your eggs in one basket.”

Get Business Continuity and Disaster Recovery for InfoSec Managers now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.