9.1. Illustration

To illustrate how all manufacturing cost budgets are put together, consider a manufacturing company called the Worth Company, which produces and markets a single product.

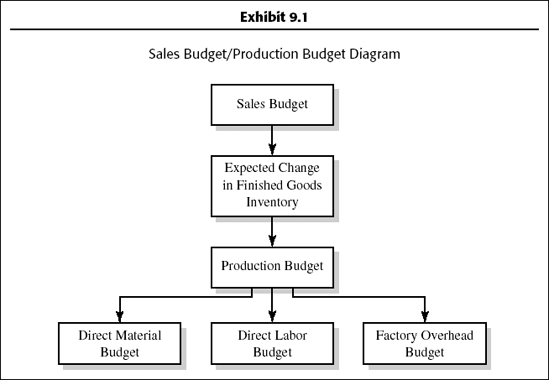

Sales Budget

The sales budget is the starting point in preparing the manufacturing budget, because estimated sales volume influences nearly all other items appearing throughout the master budget. The sales budget should show total sales in quantity and value. The expected total sales can be break-even, target income, or sales. The budget may be analyzed further by product, territory, customer, and seasonal pattern of expected sales.

Example 1

| Quarter | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | Total | |

| Expected sales in units | 800 | 700 | 900 | 800 | 3,200 |

| Unit sales price | × $80 | × $80 | × $80 | × $80 | × $80 |

| Total sales | $64,000 | $56,000 | $72,000 | $64,000 | $256,000 |

Production Budget

The production budget is a statement of the output by product and is generally expressed in units. It should take into account the sales budget, plant capacity, whether stocks are to be increased or decreased, and outside purchases. The number of units expected to be manufactured to meet budgeted sales and inventory requirements is set forth in the production budget.

The expected volume of production is determined by subtracting the estimated inventory at the beginning of the period from the sum of the units expected ...

Get Budgeting Basics and Beyond now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.