4.6. CVP Analysis with Step-function Costs

The introduction of step-function costs is somewhat more difficult than it might first appear. Ideally, we would like to be able to assume that, for any given relevant range, we could simply add together the step-function costs and the fixed costs to give us the total applicable fixed costs. We then could utilize the formula as described earlier. Unfortunately, the process is not quite that simple, as the next example illustrates.

Example 16

Amco Magazine Company publishes a monthly magazine. The company has fixed costs of $100,000 a month, variable costs per magazine of $.80, and charges $1.80 per magazine. In addition, the company also has supervisory costs. These costs behave in this way:

| Volume | Costs |

|---|---|

| 0-50,000 | $10,000 |

| 50,001-100,000 | 20,000 |

| 100,001-150,000 | 30,000 |

Amco's monthly break-even volume (number of magazines) can be calculated step by step.

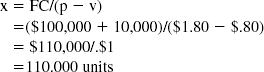

If we attempt to solve the break-even formula at the first level of fixed costs, we have this equation:

The problem with this solution is that, while the break-even volume is 110,000 magazines, the relevant range for the step-function costs was only 0-50,000 magazines. Thus, a break-even of greater than 50,000 magazines is invalid, and we must move to the next step on the step function, which gives us the next equation:

This solution is also invalid. Only when we get to the third level do we ...

Get Budgeting Basics and Beyond now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.