Yield Convexity

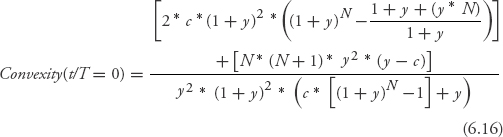

The bond convexity statistic is the second-order effect in the Taylor series expansion. Getting an equation for convexity is just a matter of more calculus and algebra; see the Technical Appendix for all the details. However, the results are complicated enough to warrant separate equations for coupon payment dates and between coupons. Equation 6.16 is the formula that applies to a coupon payment date such that t/T = 0.

Granted, there are a lot of terms in the equation, but just three variables: c, the coupon rate per period; y, the yield to maturity per period; and N, the number of periods to maturity. One simplification emerges ...

Get BOND MATH: The Theory Behind the Formulas now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.