3.2. Statistical Background

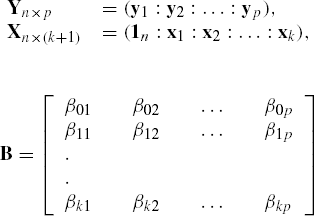

A multivariate linear model in p (possibly correlated) response variables y1,...,yp and k independent or predictor variables x1,...,xk is represented by a system of p univariate linear models

where yi, xi, and ϵi are all n by 1 vectors. The vectors yi and xi are respectively the data vectors on the variables yi and xi. These equations can compactly be represented using matrix notation as

Y=XB + ϵ, (3,2)

where

and ɛ = (ϵ1:ϵ2:... :ϵp). The vector 1n here represents an n by 1 column vector with all elements as unity. ...

Get APPLIED MULTIVARIATE STATISTICS: WITH SAS® SOFTWARE now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.