16.3. Distinguish Profit from Cash Flow

|

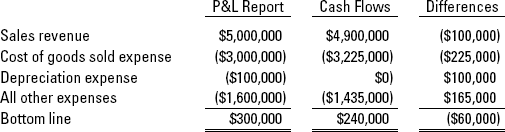

Figure 16-1 shows an example I designed to illustrate the differences between sales revenue and expenses (the accounting numbers used to measure profit) and the cash flows of the sales and expenses. Only three expenses are shown: cost of goods sold, depreciation, and one total amount for all other expenses. (Note: Reporting expenses this way is not adequate for managers in a P&L report and is not acceptable for income statements in an external financial report.)

Figure 16.1. Comparing sales and expenses and their cash flows.

Here are the ...

Get Accounting For Dummies®, 4th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.