Book III

Adjusting and Closing Entries

Check out www.dummies.com/extras/accountingaio for specifics on how to adjust your accounting records with accruals and deferrals.

Check out www.dummies.com/extras/accountingaio for specifics on how to adjust your accounting records with accruals and deferrals.

In this book…

- Choose the best depreciation method for your long-term assets. Assets are used to generate revenue, and depreciation expenses the cost of the asset as it's used in business.

- Account for interest your business pays or receives. If your business borrows or lends money, it pays or collects interest. Either way, you need to account for that interest.

- Prove out the cash to ensure that what's on paper matches the real dollar amounts in a store or office. Your cash account typically has a lot of transactions. As a result, you need to carefully account for cash to ensure that all the activity is properly recorded.

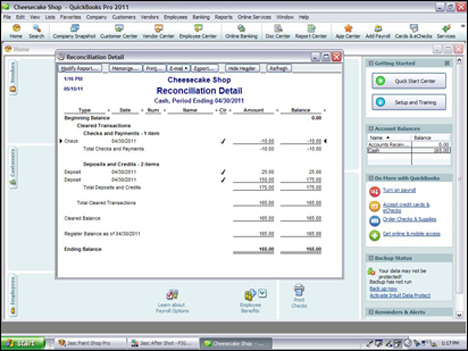

- Reconcile accounts and confirm that your journals and general ledger are correct. Reconciling your books is a great way to check your work, correct any errors, and even spot signs of fraud!

- Double-check your books by running a trial balance, correct any errors, and prepare a financial statement worksheet. A trial balance lists all your accounts and their dollar balances.

- Adjust the books in preparation of preparing financial reports. Trial balances are adjusted before being used to create financial ...

Get Accounting All-in-One For Dummies now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.